Singapore’s electricity system is built around reliability, yet it also faces a transition challenge in a land-constrained city-state. Singapore generated 60 TWh of electricity in 2024, and total electricity consumption was 58 TWh, according to the Energy Market Authority (EMA). In that same year, the industrial and commerce & services sectors each used 23 TWh, while households used 8 TWh and transport used 3 TWh. The context for Singapore low-carbon electricity imports is that the country is actively blending domestic renewable build-out, grid upgrades, and regional power trade to widen supply options while supporting emissions goals.

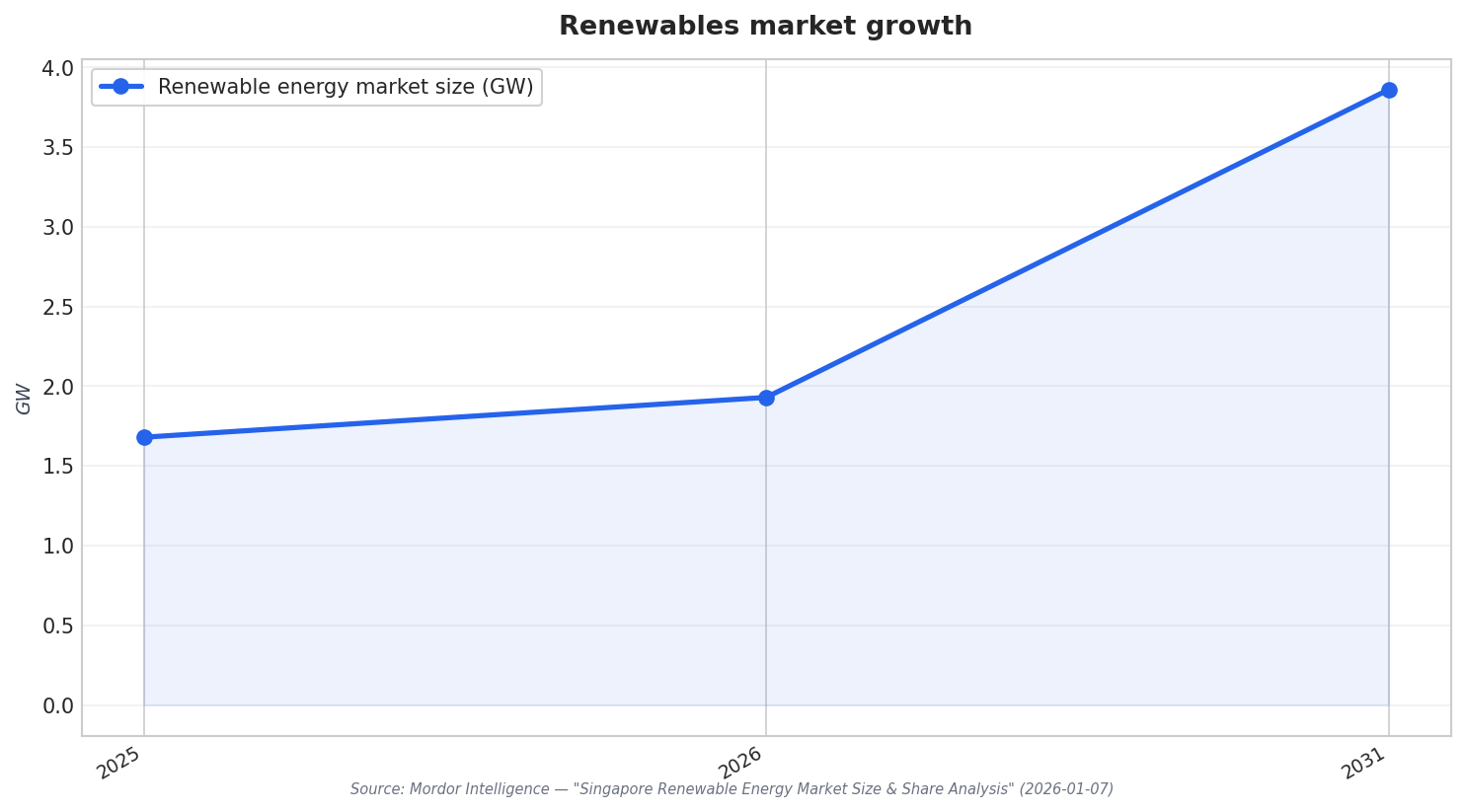

Domestic renewable growth remains central, especially solar. Mordor Intelligence estimates Singapore’s renewable energy market at 1.68 GW in 2025 and 1.93 GW in 2026, with a projection of 3.86 GW by 2031, at a 14.86% CAGR over 2026–2031. Solar led with 83.65% market share in 2025 and is forecast to be the fastest-growing technology through 2031 at a 15.38% CAGR. Grid operators are also addressing variability with storage and forecasting, including the roll-out of a 285 MWh battery system and a solar forecasting model funded by SGD 6.2 million in R&D grants.

Why Imports Matter: Capacity Targets, Projects, and the Regional Grid

Regional power trade is positioned as a major supply lever alongside local renewables. Mordor Intelligence cites regional import targets of 6 GW by 2035 as a way to add supply diversity and support Singapore’s role as a cross-border clean-power hub. S&P Global describes an agreement tied to seven projects in Indonesia’s Riau Islands and Sumatra with a combined capacity of 3.4 GW, framed as supporting Singapore’s ambition to import up to 6 GW of clean power by 2035. S&P Global also notes this 6 GW target represents one-third of the city-state’s electricity mix by 2035, attributed to an EMA target.

Imports also depend on grid readiness and governance. A Scientific Reports study (2025) finds that with strategic upgrades and smart grid technologies, Singapore’s grid can manage the variability and intermittency of renewable energy sources, including both generated and imported renewables. The same study notes Singapore’s power system has links to the Malay Peninsula, and that a planned ASEAN regional interconnection could alter grid operations and possibly make Singapore a new green energy hub. It highlights cross-border trade requirements such as harmonized regulatory frameworks and incentives that foster public–private partnerships.

Cost and market design can shape how quickly new imports scale. S&P Global reports estimates that the Singapore-Indonesia cross-border project could cost about S$300/MWh, reflecting grid charges and backup costs, and that this is approximately 17% above the prevailing retail electricity rate in Singapore. It also reports that offtakers purchasing electricity directly from the wholesale market are required to pay Renewable Energy Certificate (REC) prices of around S$130–140/MWh (per Energy estimates cited by S&P Global) for developers to recoup costs. These practical price signals sit alongside broader energy security concerns, as S&P Global notes wholesale power prices rose by more than fourfold in Singapore in 2022 from 2020 levels, amid the global energy crunch in late 2021.

What is Singapore aiming for in low-carbon electricity imports by 2035?

Which cross-border projects are highlighted as supporting Singapore’s import ambition?

How much electricity did Singapore generate and consume in 2024?

What do sources say about the cost of cross-border clean power to Singapore?